Why SMEs don't hedge, and what that costs them.

The hedging infrastructure that serves corporate treasuries is economically incompatible with SME transaction sizes. This isn't a pricing problem; it's a structural one. Bretton explains how Micro Hedging™ and the HNPL™ settlement model rebuild FX risk management around single commercial obligations rather than quarterly forecasts.

Why SMEs don't hedge, and what that costs them

There is a curious gap in the way foreign exchange risk is managed. Large corporates hedge as a matter of course. They run forecasting cycles, book forward contracts against aggregate exposure, post collateral under ISDA master agreements, and treat FX as a manageable line item in the financial statements. Small and medium enterprises, whose international payments often represent a greater share of revenue and whose margins are typically thinner, do almost none of this. They transact at spot, absorb the variance, and treat FX as weather.

This isn't because SMEs are less sophisticated. It's because the hedging infrastructure that serves corporate treasuries is, by design, economically incompatible with SME transaction sizes. A standard wholesale forward contract has a minimum notional well above the typical SME invoice. Documentation runs to dozens of pages. Credit support annexes require collateral postings that tie up working capital. Variation margin calls land unpredictably and require same-day cash response. Setup takes weeks; ongoing operation requires a treasury function the SME does not have.

Faced with these barriers, the rational choice for an SME is not to hedge. And so they don't.

The cost of not hedging

The cost of this non-hedging is real but diffuse, which is part of why it persists. A business paying a USD 10,000 invoice in thirty days faces a settlement amount that depends on spot at the payment date. If the AUD weakens by 3% in the interim, that is a 3% margin erosion on a transaction the business priced against today's rate. Over a year, across dozens of such transactions, the accumulated cost is material. It just isn't visible in any single month, and it doesn't arrive as a bill.

More fundamentally, non-hedging distorts commercial decisions. Businesses that cannot lock their input costs cannot price confidently in foreign currency. Contracts get priced with FX buffers built in, which cost the business competitiveness. Longer payment terms become risky where they should be commercially useful. Expansion into new currency corridors gets deferred. The exposure becomes a constraint on the commercial strategy, not just a cost against it.

Hedging at the wrong altitude

Why does wholesale FX infrastructure not work for smaller transactions? The answer is that it operates at the wrong altitude. A corporate treasury forecasts aggregate exposure over one to four quarters and hedges the forecast, not the individual obligations. The forward contract is sized to the forecast, dated to a convenient settlement, and maintained through quarterly roll cycles. When actual cash flows deviate from forecast, which they always do, the hedge carries basis risk: the hedge and the underlying obligations are no longer perfectly aligned.

This is acceptable at corporate scale because the absolute amounts are large enough to absorb the operational cost of forecasting, documentation, and maintenance. At SME scale, the forecasting infrastructure doesn't exist, the transaction sizes don't support the fixed costs, and the basis risk that is tolerable at corporate scale becomes the whole exposure.

The response to this mismatch, historically, has been to tell SMEs to use spot and accept the variance. We think there is a better response, which is to build hedging infrastructure designed for the transaction sizes and operating realities of the businesses using it.

Hedging one invoice at a time

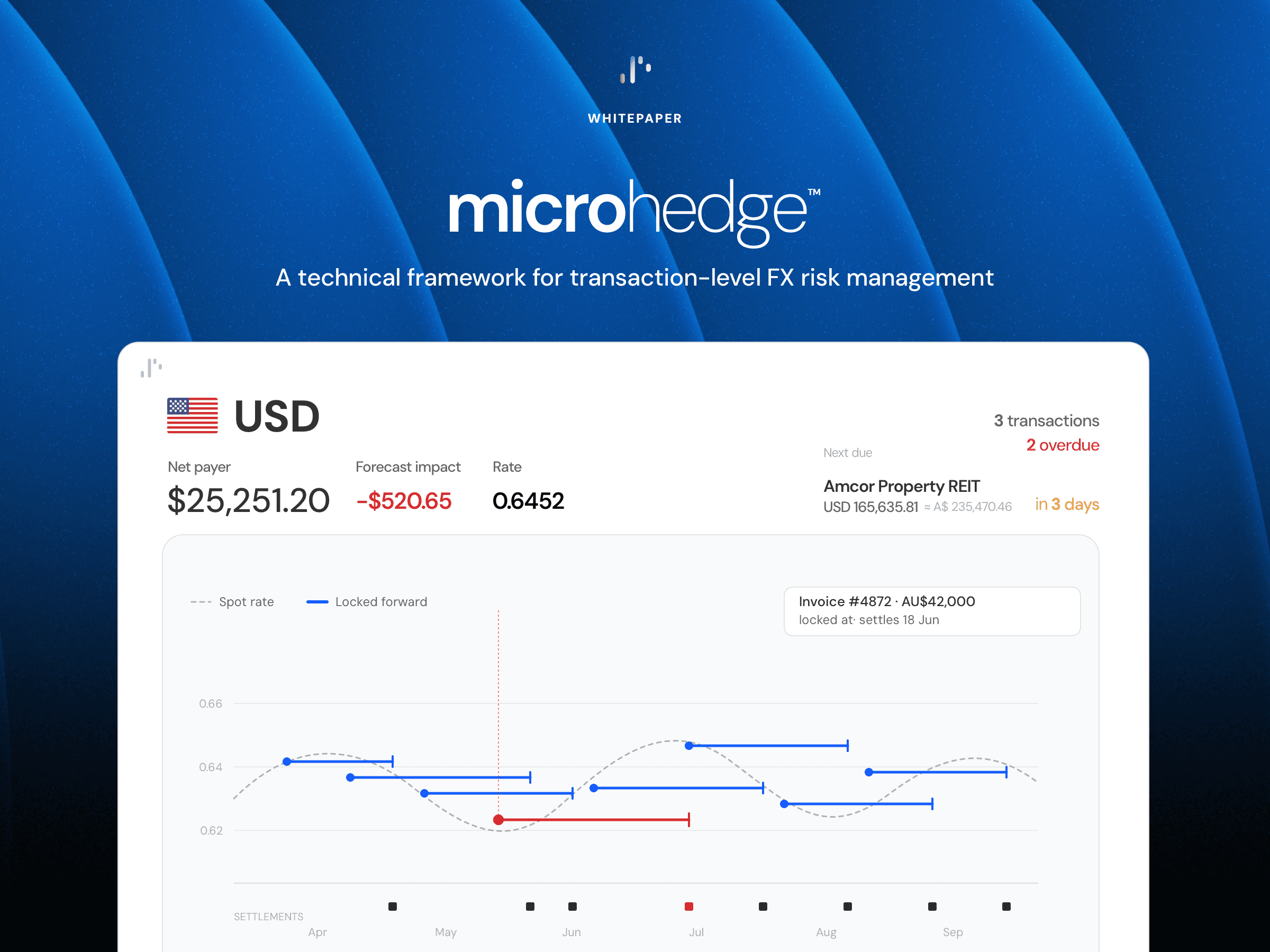

Micro Hedging™ is the framework we have developed for this. It replaces the portfolio-level forward contract with an obligation-level primitive: a forward position sized, priced, and settled against a single commercial obligation. Not a forecast of quarterly exposure. Not a rolling programme against an imagined flow. One invoice, one hedge, one settlement.

This is a structural shift. A traditional forward contract asks the business to predict its foreign-currency needs in aggregate and trust that prediction to hold. A micro-hedge™ asks only that the business knows, today, that it owes USD 10,000 in thirty days. That is a fact the business already has. The hedge is defined by reference to the invoice itself, not by reference to any forecast.

Basis risk at the client level is eliminated by construction, because the hedge and the underlying are one-to-one. The size, the value date, and the pricing all come from the obligation. There is no forecasting layer to be wrong about.

The settlement model that makes it work

Replacing the instrument is only half the problem. The other half is replacing the settlement experience. A traditional forward contract requires the client to post initial margin at trade date, respond to variation margin calls daily, and maintain collateral against the position for the life of the hedge. This is the piece of the wholesale machinery that is most structurally incompatible with SME operations, and which we have found most in need of redesign.

Micro Hedging™ settles under what we call the Hedge Now, Pay Later model, or HNPL™. The client's only obligation across the life of the hedge is a single payment in domestic currency on the settlement date, at the locked rate. No initial margin. No variation margin calls. No collateral postings. No ISDA documentation. The client accepts a rate; thirty days later, they pay one amount; the foreign currency is delivered to the beneficiary. The settlement experience is indistinguishable from a spot transfer with a deferred value date.

The wholesale margin obligations don't disappear; they are absorbed by Bretton and funded from our own infrastructure. The cost of that absorption is embedded in the all-in rate the client sees, much as the financing cost in a Buy Now Pay Later arrangement sits within the merchant price rather than surfacing as a separate charge. The client pays one rate, on one date, for one currency amount. The machinery sits behind us.

What this makes possible

The technical framework is set out in full in the accompanying whitepaper. What matters commercially is what the framework makes possible.

It makes possible forward-rate protection on invoices of any size, including the small invoices that wholesale infrastructure has always refused. It makes possible fixed-price quoting in foreign currency for services that are delivered over weeks rather than quarters. It makes possible the expansion of commercial relationships into currency corridors that were previously too small to hedge and therefore too risky to price. It makes possible a finance function in which FX is a solved problem rather than an accepted variance.

None of this requires the SME to change how they operate. It requires the hedging infrastructure to change how it serves them. That is what we have built.

The full technical framework, including the conceptual model, the lifecycle of a single hedge, the rate construction, and the HNPL™ settlement model, is set out in our whitepaper, Micro Hedging™: A technical framework for transaction-level FX risk management. If you are responsible for FX risk at a business that has previously accepted variance because wholesale hedging did not fit, we would encourage you to read it.